SMARTTRAC HIGHLIGHTS:

SMARTTRAC HIGHLIGHTS:

- Bankruptcy, Short Sale, Deed-in-Lieu: 12 months seasoning (from date of event)

- Multiple 30 day lates on housing payments allowed

- 620 min. FICO – all occupancy types

- $1M Cash Out at 80% LTV, $1M Cash in hand

- Up to 15 Financed Properties

- Up to 45% Debt to Income Ratios; 50% with 3 months of additional reserves

- Appraisal Transfers Permitted

- Fixed 30; ARM 5/1, 7/1, 10/1 – all with optional Interest Only

- No Pre-Payment Penalties

- 80% LTV Purchase/Rate Term; 75% Cash Out

Program Summary:

The SmartTrac Product is designed for strong credit quality borrowers with a credit event or other isolated lapse in their credit performance that may preclude qualification for another program. Credit events include, without limitation, bankruptcy, foreclosure, short sale or any other isolated instance of breach in an otherwise acceptable credit pattern. Other isolated lapses in credit performance would be characterized as a period of slow payments on their credit, such as 30 or 60 day delinquencies resulting from isolated circumstances. All borrowers must exhibit an acceptable recent credit history (as defined within this product profile) and provide a written explanation for derogatory credit events. Multiple credit events that are not a result of the same cause are not permitted (Ex: Borrower who filed bankruptcy on multiple occasions).

Eligible Transactions:

• Purchase• Rate & Term (Limited Cash-out) Refinance

• Cash-out Refinance

Ineligible Transactions:

Unacceptable loan types include but are not limited to the following, provided, however, that in the event that any of these limitations would violate the requirements of the Equal Credit Opportunity Act or the Fair Housing Act, the provisions of those laws and implementing regulations are controlling:

• Any loan that meets an agency, state or a federal definition of a high cost loan

• Borrowers with diplomatic immunity or otherwise excluded from U.S. jurisdiction.

• Bridge loans

• Cross-collateralization or Blanket loans, covering multiple properties

• Deed-Restricted Properties (exceptions will be considered on a case-by-case basis)

• Flip transactions (multiple private transfer in the last 12 months; see Property Flips/Rapid Appreciation for more details)

• Foreclosure bailouts of any kind. (An arms-length purchase of a short sale is not deemed a foreclosure bailout.)

• Land trusts in the state of Illinois

• Leaseholds secured by Indian/Tribal lands

• Lease-Purchase Options

• Loans to fund escrows for work completion except as provided in this guide

• Loans to mortgage loan officers

• Loans with any fraudulent activities including but not limited to straw borrowers, straw buyers, builder/seller bailout plans, multiple property payment skimming, which typically involves investors who purchase investment properties with seller carry back financing and collect rents but do not make the mortgage loan payments.

• Model Home Lease-Backs

• Mortgage Credit Certificates (MCC)

• Refinancing of a subsidized loan, including loans subsidized by Habitat for Humanity, U.S. Department of Agriculture, FHA with a recapture or any city/county grant.

• Reverse 1031 Exchanges

• Temporary Buydowns

Maximum # of Financed Properties:

Borrower(s) may own no more than fifteen (15) financed properties including the subject property, unless the current principal residence is pending sale and meets the requirements of this product profile. The borrower may own additional real estate if it is owned free and clear. The following property types are not subject to these limitations, even if the borrower is personally obligated on a mortgage on the property: 1) commercial real estate, 2) multifamily property consisting of more than four units, 3) ownership in a timeshare, 4) ownership of a vacant lot (residential or commercial), or 5)ownership of a manufactured home on a leasehold estate not titled as real property (chattel lien on the home). Loan files must include full PITIA (principal, interest, taxes, insurance, applicable association dues and/or assessments) for all REO listed on the 1003. Refer to Cash Reserves for additional requirements.

Occupancy:

Eligible occupancy types include:

• Primary residences for 1-4 unit properties

• Second Homes – 1-2 Unit only o For 2 unit second homes, one unit must be available for the borrower’s exclusive use, no rental or time-sharing arrangements in the borrower’s exclusive unit. Must be suitable for year round use. Must be located in a recognized vacation area typical for second home properties (e.g., beach, ski, golf, resort). Must be a reasonable distance from borrower’s current owner-occupied property

• Investment or Non-Owner Occupied – 1-4 Units

Ineligible Borrowers:

• Borrowers with diplomatic immunity or otherwise excluded from U.S. jurisdiction

• Borrowers who are citizens and not employed in the U.S.

• Foreign Nationals

• Land Trusts

• Borrowers whose qualifying income is not likely to continue for at least 3 years (e.g., a bonus or an inheritance)

• Properties vested in an LLC or Corporation (title must be taken as an individual)

• Borrowers with any ownership in a business that is federally illegal, regardless if the income is not being considered for qualifying

Maximum Acreage:

Properties are limited to 20 acres. Acreage and land value must be typical and common for the subject’s market. The appraiser must indicate the total acreage as well as provide data which indicates that like-size properties with similar land values are typical and common in the subject area’s market. It is not acceptable to have property appraised with only 20 acres in order to meet eligibility.

Condos:

All loans secured by condos must be reviewed by the Lender prior to approval.

Warrantable Condos:

• Both FNMA Condo Project Manager (CPM) and FNMA Limited Review are allowed

• Detached Condo units that are Principal Residences may be processed with Limited Review

• If project is currently FNMA approved, a HOA Certification is still required.

• New projects are not eligible for Limited Review

• New or newly converted projects in Florida are eligible with a Full Review and must meet the following: 1) Maximum LTV/CLTV/HCLTV 60%, 2) Maximum Lender exposure in any one project is limited to 20%

Non-Warrantable Condos:

• The FNMA investment property concentration limits (i.e., the percentage of non-owner occupied properties within a project) do not apply

• Minimum 50% of units in project (or subject legal phase, considered with prior legal phases) must be sold or under contract. 50% requirement is cumulative and for each individual phase

• Single Entity Ownership Exception: 1) Projects in which a single entity (the same individual, investor group, partnership, or corporation) owns up to and including 25% of the total number of units in the project are permitted

Ineligible Property Types:

Acreage greater than 20 acres (appraisal must include total acreage) • Agricultural zoned property • Commercial Enterprises (e.g. Bed and Breakfast, Boarding House, Hotel) • Condotels • Co-ops • Geodesic Domes, Berms, Earth homes • Hobby Farms • Income producing properties with acreage • Leaseholds • Log homes • Manufactured/Mobile, Modular, or Factory Built Homes • Projects with insufficient Flood Insurance – Borrower supplemented is not permitted • Properties appraised with a property condition of C5 or worse • Properties held in a business name • Properties located adjacent to or containing environmental hazards • Properties Purchased Through Auctions • Properties subject to oil and/or gas leases (may be eligible on a case-by-case basis) • Properties vested in an LLC or Corporation (title must be taken as an individual) • Properties with less than 750 square feet of living area • Timeshares • Unimproved Land and property currently in litigation • Unique properties • Working farms, ranches or orchards • Zoning violations including residential properties zoned commercial

Employment:

Employment must be reviewed for stability and continuity, with at least a two year history in the same job or jobs in the same or related field. Other circumstances may also be acceptable as outlined in this section. In all instances the source of the borrower’s income must align with their overall employment history and profile.

Income:

All income documentation must be dated within 90 days of the date the Note is signed. Full Income Documentation is required, which includes:

Wage Earners:

• Paystubs and W-2s or Personal tax returns, signed and dated, plus business tax returns when the borrower has 25% or more ownership interest in the business

• A 4506-T, signed at application and closing, is required for all transactions. IRS Tax Transcripts are required for the most recent two years.

• A Verbal Verification of Employment is required for all borrowers

Self Employed:

A borrower with a 25% or greater ownership interest in a business is considered self-employed. Self-Employed Borrowers are permitted with a minimum 2-year history.

Documentation Requirements:

YTD Q1 P&L/Balance Sheet required for loans with note dates 5/1 to 7/31

YTD Q2 P&L/Balance Sheet required for loans with note dates 8/1 to 10/31

YTD Q3 P&L/Balance Sheet required for loans with note dates 1/1 to 1/31

Full year P&L/Balance Sheet required for loans with note dates 2/1 to 4/30 AND filed returns have not been provided

Residual Income (Disposable Income):

For loans with DTI > 43% residual income requirements must be met. Residual income equals Gross Qualifying Income less Monthly Debt (as included in the debt-to-income ratio).

Eligible Income Sources

Annuity and/or Pension Income income may be used as qualifying income if it is properly documented and is expected to continue for at least three years. Acceptable documentation includes: Most recent award letter; or Most recent 2 years 1099; and copy of the bank statement showing current receipt

Asset Based Income (Asset Amortization):

Asset amortization is a calculation used to generate a monthly income stream from a borrower’s personal assets. It can be combined with other income sources. There is no age restriction. The following requirements must be met:

Eligible Assets (must be readily available to borrower(s) with no penalties or limitations):

Ineligible Assets

Asset Amortization Calculation

Down payment, closing costs and any necessary adjustments as outlined above must be subtracted from eligible asset sources to determine net available assets. Net available assets are divided by the term of the subject mortgage to calculate a qualifying asset based income.

EXAMPLE:

Savings Account Balance $200,000 ($200,000 Usable toward calculation)

Stock Fund Balance $100,000 ($90,000 Usable toward calculation)

Mutual Fund Balance $20,000 ($18,000 Usable toward calculation)

Down Payment and Closing Costs = $50,000

Net eligible assets = $308,000 – $50,000 = $258,000

Term of mortgage = 360 months

Asset Amortization Calculation = $258,000/360 = $716.66 monthly income

Reserves:

The required number of months of reserves is dependent on factors such as but not limited to the occupancy, loan purpose, type of property, and loan amount. The monthly housing expense for purposes of determining reserves includes the following:

Acceptable Assets:

Cash Reserves:

Contact Loan Officer for information on the following other types of income:

Boarder Income

Borrowers Regularly Scheduled for less than 40 hours

Bonus, Incentive & Overtime Income

Capital Gains

Child Support, Alimony, Maintenance Income

Commission

Disability

Dividend and/or Interest Income

Employment Offers

Employment by a Relative/Family Business

Foreign Income

Foster Care Income

Installment Sales & Land Contracts

Military Income

Mortgage Differential Income

Notes Receivable Income

Non-Taxable Income

Part-Time, Second Job

Relocating Life Partners, Trailing Co-Borrowers

Rental Income

Retirement or Social Security Income

Royalty Income

Seasonal Income

Stock Options

Trust Income

VA Survivors' Benefits/Dependent Care

The SmartTrac Product is designed for strong credit quality borrowers with a credit event or other isolated lapse in their credit performance that may preclude qualification for another program. Credit events include, without limitation, bankruptcy, foreclosure, short sale or any other isolated instance of breach in an otherwise acceptable credit pattern. Other isolated lapses in credit performance would be characterized as a period of slow payments on their credit, such as 30 or 60 day delinquencies resulting from isolated circumstances. All borrowers must exhibit an acceptable recent credit history (as defined within this product profile) and provide a written explanation for derogatory credit events. Multiple credit events that are not a result of the same cause are not permitted (Ex: Borrower who filed bankruptcy on multiple occasions).

Eligible Transactions:

• Purchase• Rate & Term (Limited Cash-out) Refinance

• Cash-out Refinance

Ineligible Transactions:

Unacceptable loan types include but are not limited to the following, provided, however, that in the event that any of these limitations would violate the requirements of the Equal Credit Opportunity Act or the Fair Housing Act, the provisions of those laws and implementing regulations are controlling:

• Any loan that meets an agency, state or a federal definition of a high cost loan

• Borrowers with diplomatic immunity or otherwise excluded from U.S. jurisdiction.

• Bridge loans

• Cross-collateralization or Blanket loans, covering multiple properties

• Deed-Restricted Properties (exceptions will be considered on a case-by-case basis)

• Flip transactions (multiple private transfer in the last 12 months; see Property Flips/Rapid Appreciation for more details)

• Foreclosure bailouts of any kind. (An arms-length purchase of a short sale is not deemed a foreclosure bailout.)

• Land trusts in the state of Illinois

• Leaseholds secured by Indian/Tribal lands

• Lease-Purchase Options

• Loans to fund escrows for work completion except as provided in this guide

• Loans to mortgage loan officers

• Loans with any fraudulent activities including but not limited to straw borrowers, straw buyers, builder/seller bailout plans, multiple property payment skimming, which typically involves investors who purchase investment properties with seller carry back financing and collect rents but do not make the mortgage loan payments.

• Model Home Lease-Backs

• Mortgage Credit Certificates (MCC)

• Refinancing of a subsidized loan, including loans subsidized by Habitat for Humanity, U.S. Department of Agriculture, FHA with a recapture or any city/county grant.

• Reverse 1031 Exchanges

• Temporary Buydowns

Maximum # of Financed Properties:

Borrower(s) may own no more than fifteen (15) financed properties including the subject property, unless the current principal residence is pending sale and meets the requirements of this product profile. The borrower may own additional real estate if it is owned free and clear. The following property types are not subject to these limitations, even if the borrower is personally obligated on a mortgage on the property: 1) commercial real estate, 2) multifamily property consisting of more than four units, 3) ownership in a timeshare, 4) ownership of a vacant lot (residential or commercial), or 5)ownership of a manufactured home on a leasehold estate not titled as real property (chattel lien on the home). Loan files must include full PITIA (principal, interest, taxes, insurance, applicable association dues and/or assessments) for all REO listed on the 1003. Refer to Cash Reserves for additional requirements.

Occupancy:

Eligible occupancy types include:

• Primary residences for 1-4 unit properties

• Second Homes – 1-2 Unit only o For 2 unit second homes, one unit must be available for the borrower’s exclusive use, no rental or time-sharing arrangements in the borrower’s exclusive unit. Must be suitable for year round use. Must be located in a recognized vacation area typical for second home properties (e.g., beach, ski, golf, resort). Must be a reasonable distance from borrower’s current owner-occupied property

• Investment or Non-Owner Occupied – 1-4 Units

Ineligible Borrowers:

• Borrowers with diplomatic immunity or otherwise excluded from U.S. jurisdiction

• Borrowers who are citizens and not employed in the U.S.

• Foreign Nationals

• Land Trusts

• Borrowers whose qualifying income is not likely to continue for at least 3 years (e.g., a bonus or an inheritance)

• Properties vested in an LLC or Corporation (title must be taken as an individual)

• Borrowers with any ownership in a business that is federally illegal, regardless if the income is not being considered for qualifying

Maximum Acreage:

Properties are limited to 20 acres. Acreage and land value must be typical and common for the subject’s market. The appraiser must indicate the total acreage as well as provide data which indicates that like-size properties with similar land values are typical and common in the subject area’s market. It is not acceptable to have property appraised with only 20 acres in order to meet eligibility.

Condos:

All loans secured by condos must be reviewed by the Lender prior to approval.

Warrantable Condos:

• Both FNMA Condo Project Manager (CPM) and FNMA Limited Review are allowed

• Detached Condo units that are Principal Residences may be processed with Limited Review

• If project is currently FNMA approved, a HOA Certification is still required.

• New projects are not eligible for Limited Review

• New or newly converted projects in Florida are eligible with a Full Review and must meet the following: 1) Maximum LTV/CLTV/HCLTV 60%, 2) Maximum Lender exposure in any one project is limited to 20%

Non-Warrantable Condos:

• The FNMA investment property concentration limits (i.e., the percentage of non-owner occupied properties within a project) do not apply

• Minimum 50% of units in project (or subject legal phase, considered with prior legal phases) must be sold or under contract. 50% requirement is cumulative and for each individual phase

• Single Entity Ownership Exception: 1) Projects in which a single entity (the same individual, investor group, partnership, or corporation) owns up to and including 25% of the total number of units in the project are permitted

Ineligible Property Types:

Acreage greater than 20 acres (appraisal must include total acreage) • Agricultural zoned property • Commercial Enterprises (e.g. Bed and Breakfast, Boarding House, Hotel) • Condotels • Co-ops • Geodesic Domes, Berms, Earth homes • Hobby Farms • Income producing properties with acreage • Leaseholds • Log homes • Manufactured/Mobile, Modular, or Factory Built Homes • Projects with insufficient Flood Insurance – Borrower supplemented is not permitted • Properties appraised with a property condition of C5 or worse • Properties held in a business name • Properties located adjacent to or containing environmental hazards • Properties Purchased Through Auctions • Properties subject to oil and/or gas leases (may be eligible on a case-by-case basis) • Properties vested in an LLC or Corporation (title must be taken as an individual) • Properties with less than 750 square feet of living area • Timeshares • Unimproved Land and property currently in litigation • Unique properties • Working farms, ranches or orchards • Zoning violations including residential properties zoned commercial

Employment:

Employment must be reviewed for stability and continuity, with at least a two year history in the same job or jobs in the same or related field. Other circumstances may also be acceptable as outlined in this section. In all instances the source of the borrower’s income must align with their overall employment history and profile.

Income:

All income documentation must be dated within 90 days of the date the Note is signed. Full Income Documentation is required, which includes:

Wage Earners:

• Paystubs and W-2s or Personal tax returns, signed and dated, plus business tax returns when the borrower has 25% or more ownership interest in the business

• A 4506-T, signed at application and closing, is required for all transactions. IRS Tax Transcripts are required for the most recent two years.

• A Verbal Verification of Employment is required for all borrowers

Self Employed:

A borrower with a 25% or greater ownership interest in a business is considered self-employed. Self-Employed Borrowers are permitted with a minimum 2-year history.

Documentation Requirements:

- Two years of personal and business tax returns for all businesses owned with all applicable. Tax schedules are required. Both years must be evaluated to derive a qualifying income; borrowers with declining income will be carefully scrutinized. Includes, as applicable, K-1s, Form 1065, 1120s, Schedule E, etc.

YTD Q1 P&L/Balance Sheet required for loans with note dates 5/1 to 7/31

YTD Q2 P&L/Balance Sheet required for loans with note dates 8/1 to 10/31

YTD Q3 P&L/Balance Sheet required for loans with note dates 1/1 to 1/31

Full year P&L/Balance Sheet required for loans with note dates 2/1 to 4/30 AND filed returns have not been provided

- A year-to-date (YTD) Profit and Loss (P&L) Statement and Balance Sheet is required for all businesses where income is used for qualifying and/or for businesses that show a loss. The P&L may be audited or unaudited

Residual Income (Disposable Income):

For loans with DTI > 43% residual income requirements must be met. Residual income equals Gross Qualifying Income less Monthly Debt (as included in the debt-to-income ratio).

Eligible Income Sources

Annuity and/or Pension Income income may be used as qualifying income if it is properly documented and is expected to continue for at least three years. Acceptable documentation includes: Most recent award letter; or Most recent 2 years 1099; and copy of the bank statement showing current receipt

Asset Based Income (Asset Amortization):

Asset amortization is a calculation used to generate a monthly income stream from a borrower’s personal assets. It can be combined with other income sources. There is no age restriction. The following requirements must be met:

- Available for Primary Residence and Second Homes Only

- Borrower and Co-Borrower must be individual or co-owners of all asset accounts with no other account holders listed on the documentation

- 100% of eligible assets must be verified and will be amortized over the term of the loan (e.g., 360 months for a 30 year loan, 180 months for a 15 year loan)

- All assets must be in a U.S. financial institution—No Foreign Assets

- The sum of eligible assets as defined are net of any discounts and minus any funds used for closing and/or minimum reserves required for the program.

- Other reported earnings from Capital Gains or Interest/Dividend may not be used if Asset based income is utilized

Eligible Assets (must be readily available to borrower(s) with no penalties or limitations):

- Bank Deposits – Checking, Saving, Money Market accounts = 100%

- Investment Account: May be comprised of publicly traded stocks, bonds and/or mutual funds = 90% (stock options not allowed)

- Retirement Accounts: 401(K) plans or IRA, SEP or KEOGH accounts = 80% (IRA borrower must be at least 59 1/2; Eligible only if distributions have not been set up

- Any outstanding loan or margin accounts should be backed out of the investment accounts balance.

- No privately held stock or non-regulated financial companies

Ineligible Assets

- Business funds including personal accounts used for self-employed income calculation

- Non-liquid assets (automobiles, artwork, etc.)

- Any life insurance

- Any type of UTMA or custodial account for minors

- Bitcoin or other digital currency

Asset Amortization Calculation

Down payment, closing costs and any necessary adjustments as outlined above must be subtracted from eligible asset sources to determine net available assets. Net available assets are divided by the term of the subject mortgage to calculate a qualifying asset based income.

EXAMPLE:

Savings Account Balance $200,000 ($200,000 Usable toward calculation)

Stock Fund Balance $100,000 ($90,000 Usable toward calculation)

Mutual Fund Balance $20,000 ($18,000 Usable toward calculation)

Down Payment and Closing Costs = $50,000

Net eligible assets = $308,000 – $50,000 = $258,000

Term of mortgage = 360 months

Asset Amortization Calculation = $258,000/360 = $716.66 monthly income

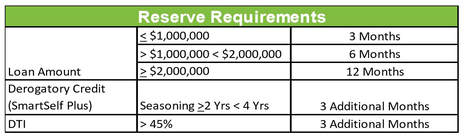

Reserves:

The required number of months of reserves is dependent on factors such as but not limited to the occupancy, loan purpose, type of property, and loan amount. The monthly housing expense for purposes of determining reserves includes the following:

- Principal and interest (P&I);

- Hazard, flood, and mortgage insurance premiums (as applicable)

- Real estate taxes

- Ground rent

- Special assessments

- Any owners’ association dues (including utility charges that are attributable to the common areas, but excluding any utility charges that apply to the individual unit)

- Any monthly co-op corporation fee (less the pro rate share of the master utility charges for servicing individual units that is attributable to the borrower’s unit)

- Any subordinate financing payments on mortgages secured by the subject property.

Acceptable Assets:

- Checking & Savings: 100% of the funds held in a checking or savings account may be used for the down payment, closing costs, and financial reserves. Any indications of borrowed funds must be investigated. They include recently opened accounts, recent large deposits, or account balances that are considerably greater than the average balance over the previous few months. A written explanation of the source of funds from the borrower must be obtained and the funds must be verified. Funds held jointly with a non-borrowing spouse are considered the Borrower’s funds.

- Business Assets: If business funds are used for down payment, closing costs and/or reserves the following requirements must be met: The borrower must be the sole proprietor or 100% owner of the business. A maximum of 50% of the account balance may be used towards down payment, closing costs and reserves. Large or irregular deposits must be explained and documented. Large deposits are deposits greater than 50% of the loans qualifying income. The Underwriter will review the tax returns of the business to determine any withdrawal of the funds will not have a negative impact on the business. Any significant withdrawal should be considered in relation to the overall strength of the borrower’s company. Funds deposited from the business into the borrower’s personal account prior to loan application are considered personal funds. Funds should be sourced.

- Stocks, government bonds, and mutual funds are acceptable sources of funds for the down payment, closing costs and reserves provided their value can be verified. Stock options may be an acceptable source of funds, but only for down payment and closing costs.

- Funds disbursed from a borrowers trust account are an acceptable source for the down payment, closing costs and reserves provided the borrower has immediate access to the funds.

- Vested funds from individual retirement accounts (IRA/Keogh accounts) and tax-favored retirement savings accounts (401(k) accounts) are acceptable sources of funds for down payment, closing costs, and reserves.

- Borrowed funds secured by an asset are an acceptable source of funds for the down payment and closing costs since the borrowed funds represent a return of equity. Assets that may be used to secure funds include: Automobile, Artwork, Collectibles, Real estate, Financial assets (Savings/Checking/CD accounts/Stocks/Bonds/401k.

- Gift Funds and Gifts of Equity are permissible sources of funds to be used towards a borrower’s down payment and closing costs. • Borrower must have a minimum 5% of their own funds into the transaction unless the LTV/CLTV is 80% or less. Maximum LTV/CLTV for Gift of Equity transaction is 75%. Primary residence transactions only. Subordinate Financing is not permitted. Gift funds cannot be used for reserves. Must be from an immediate family member.

Cash Reserves:

- Maximum amount of reserves required is 15 months

- For rate and term refinance transactions reserve requirements above are not required for primary and secondary residences that meet the following: 1)Maximum Loan Amount $1,500,000 2) 0X30X12 lates on all mortgages 3) Housing payment is decreasing on the subject property 4) SmartSelf Plus Only- 3 months reserves for derogatory credit applies 5) Borrowers who own additional real estate must have: 1) 2 months of reserves for each additional financed property owned including properties that are pending sale and will not be sold prior to the subject transaction closing. 2) The PITIA is based on each individual properties respective PITIA.

- SmartEdge Plus: Cash in hand from a cash-out refinance may be used to satisfy reserve requirements

Contact Loan Officer for information on the following other types of income:

Boarder Income

Borrowers Regularly Scheduled for less than 40 hours

Bonus, Incentive & Overtime Income

Capital Gains

Child Support, Alimony, Maintenance Income

Commission

Disability

Dividend and/or Interest Income

Employment Offers

Employment by a Relative/Family Business

Foreign Income

Foster Care Income

Installment Sales & Land Contracts

Military Income

Mortgage Differential Income

Notes Receivable Income

Non-Taxable Income

Part-Time, Second Job

Relocating Life Partners, Trailing Co-Borrowers

Rental Income

Retirement or Social Security Income

Royalty Income

Seasonal Income

Stock Options

Trust Income

VA Survivors' Benefits/Dependent Care